Faraz Rupani and Omkar Hande

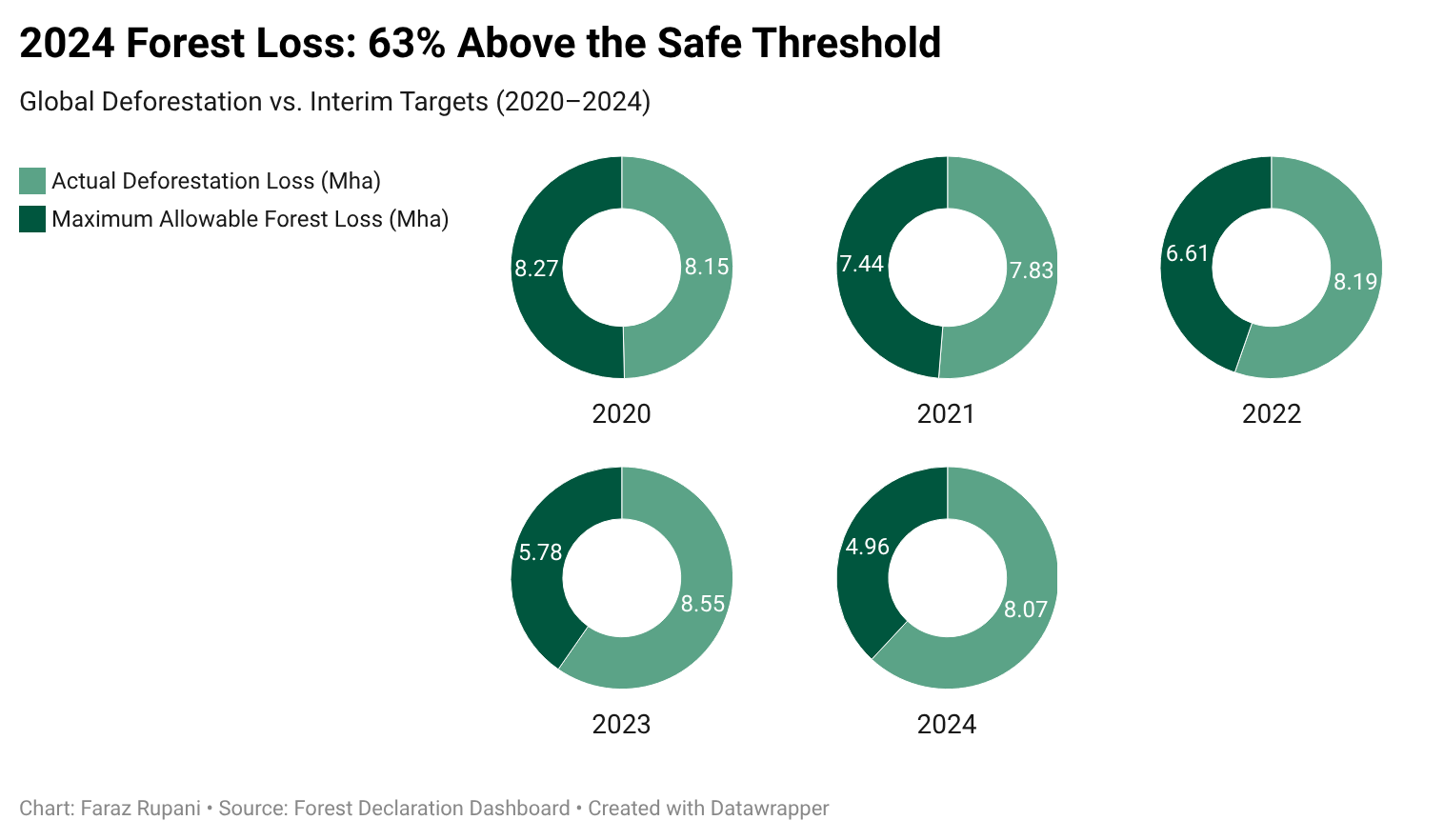

Forests cover 30 per cent of Earth, and are vital for climate stability. In 2024, the world lost nearly 8.1 million hectares of forest, 63 per cent above the safe limits. Over the last decade, about 86 per cent of global deforestation has been driven by permanent agriculture. Behind these numbers lies an under-acknowledged driver of environmental crimes generating USD 281 billion annually, with more than half coming from forestry crimes such as illegal logging, paving way to expand agricultural land.

The global south countries who have been at the center of climate hazards have begun to understand the perfunctory courtesy shown by the global north towards their climate finance obligations. The latest COP30 proceedings also gave a major signal to the developing countries that the UN and its affiliated organisations are in a flux, with COPs now increasingly moving towards becoming a lobbying arena rather than a climate conference.

The Tropical Forest Investment Fund (TFIF) announced at COP30 nonetheless emerged as a bright spot for forest protection, at least rhetorically. TFIF is not a first of its kind forest fund; yet is remarkably different from existing funds. The fund, designed as an endowment-style mitigation fund, focuses on long-term conservation and remuneration, and is intended to become one of the largest environmental finance instruments supporting the conservation of tropical forests globally.

TFIF at its core is a USD 125 billion endowment-style mitigation fund to support long term forest maintenance and recovery across eligible Tropical Forest Countries (TFCs) (covering parts of South America, Africa, Southeast Asia and Australia). Unlike traditional climate finance models that rely on annual donor pledges, TFIF would establish a permanent capital base funded by both private and public investors.

The fund would consist of USD 25 billion in sponsor capital provided by sovereign countries, with repayment beginning after a 10-year grace period. This would be complemented by a USD 100 billion senior debt tranche raised from the private sector. Historically, the private sector has been cautious in forest finance due to a long time horizon and the mixed performance of past initiatives. TFIF addresses this by creating structured, investment grade vehicles designed to provide practicable returns.

The full USD 125 billion fund would then be invested in long-dated fixed-income assets to build a diversified, and sustainable portfolio. The target is to achieve a AAA rating and generate annual return of 2.5% to 3.0% above the cost of capital.

The income generated would follow a clear priority structure: returns would first service the private debt, then repay sponsor capital, and finally provide performance based payment to Tropical Forest countries (TFCs). Eligible countries would receive USD 4 per hectare for verified forest protection and maintenance. TFCs would pay at least 20% of the receipts to Indigenous Peoples and Local Communities (IPLCs) while the rest to support national conservation projects.

The fund, although modelled differently with unique attributes, raises broader sets of questions: Are endowment-style mitigation financing signalling a shift towards permanent capital vehicles? Will this experiment potentially become the new normal in climate finance and will adaptation financing finally resurgence?

Latest data shows that mitigation funds have grown to USD 1.8 trillion, highest ever, while adaptation financing continues to shrink. An assessment of 30 existing financial mechanisms for forest-related finance reveal that 31 per cent of committed forest finances are yet to be disbursed, while public sources account for 91 per cent of global forest finances.

Despite the fund’s early enthusiasm due to its structure, particularly from major tropical forests such as Brazil and Indonesia, which each pledged USD 1 billion, sovereign commitments have fallen short of expectations. To date, the fund has secured only USD 6.7 billion in total pledges from sovereign countries. This is well below the level needed to catalyze large scale private investments.

Norway has committed an additional USD 3 billion but only once total sovereign capital reaches USD 10 billion. While interest remains strong in principle, reaching its initial sovereign contribution capital threshold has proven to be a hurdle.

So, why are countries still not committing their investments to endowment-style financing?

Several factors explain the slow pace of sovereign commitments. Firstly, the sheer scale of investment and long payback period make countries hesitant, especially as major economies are in flux amid global uncertainties. Secondly, the global growth is expected to slow, according to the IMF, forcing countries to adopt a stimulative fiscal stance to protect their own interests.

Thirdly, the United States’s withdrawal from the Paris Agreement and United Nations affiliated organisations has already pushed wealthy countries to realign their budgets to fund existing climate projects. This hesitancy also delays garnering investments from institutional investors, as sponsor capital is primarily seen as the first-loss cushion delaying the process of TFIF further.

Concerns about TFIF are not only about funding, other significant risks lie in the trade-offs on the ground. Armed groups earn around USD 4 out of every USD 10 from illicit environmental activities. A minimum dollar-per-hectare for conservation to the indigenous communities responsible for managing forests is insufficient to compete with income from illegal operations. This imbalance could make communities vulnerable to pressure or coercion from armed groups, potentially drawing them into environmental crimes instead of forest protection.

Even though the TFIF’s idea looks promising, it is too early to conclude whether endowment-style mitigation funds could transform climate finance. Long-dated fixed income assets may attract institutional investors, however securing upfront capital remains challenging in the current economic and political landscape. Market volatility and limited transfer of benefit to indigenous communities could undermine the very mechanism these funds rely on. Meanwhile, the widening imbalance between mitigation and adaptation financing continues to grow, as both private and public investors continue to downplay adaptation financing raising questions about the overall allocation of climate funding.

Ultimately, TFIF’s success will hinge not just on clever financial engineering but on its ability to deliver absolute returns to investors and communities while navigating political risks, market risks, rising environmental crime, and illegal profits that may outpace incentives for conservation. If the Global South bet on endowment styled mitigation financing succeeds, it could reduce dependence on global north for financing in the long run. Without renewed investments in adaptation financing, the TFIF’s impact would be partial and largely symbolic, and even the strongest endowments may fail to deliver meaningful outcomes in the longer-run.

Summing Up

- Global Forest Loss and Drivers of Deforestation: In 2024, nearly 8.1 million hectares of forest were lost, driven mainly by permanent agriculture, with illicit forestry activities generating USD 281 billion annually.

- Shift in Climate Finance and the Future of COP Conferences: Developing countries are growing skeptical of climate finance commitments from the global north, as COP30 indicates a move toward lobbying rather than genuine climate action.

- Structure of the Tropical Forest Investment Fund (TFIF): TFIF is a USD 125 billion endowment-style fund aimed at supporting long-term tropical forest conservation through permanent capital from governments and private investors.

- Financial Model and Investment Strategy of TFIF: The fund plans to invest USD 25 billion in sponsor capital and raise USD 100 billion via private sector debt, targeting a AAA rating and annual returns of 2.5-3%, with profits supporting forest countries and communities.

- Challenges and Risks to TFIF’s Success and Broader Climate Goals: TFIF faces hurdles such as slow sovereign commitments, economic uncertainties, illicit activities affecting forests, and the need for balanced mitigation and adaptation funding, which may limit its impact.